Your offer letter says $72,000. Your first paycheck says something very different. That gap — between what you earn and what you actually keep — is where most financial mistakes are born. Annual income is the foundation of every major money decision you’ll make: getting a mortgage, filing taxes, building a retirement plan. This guide breaks down exactly what annual income means, what counts toward it, how to calculate yours, and what that number actually unlocks.

What You’ll Learn

- The difference between gross and net annual income

- Every income source that counts (including ones most people miss)

- Step-by-step calculations for salaried, hourly, and self-employed workers

- How your annual income affects taxes, loans, and retirement

What Is Annual Income?

Annual income is the total money you earn or receive from all sources over a 12-month period. It’s not just your salary. It includes freelance payments, rental income, dividends, bonuses — any dollar that flows toward you in a year.

Most people interact with two versions of this number:

- Gross annual income — everything you earn, before taxes or deductions

- Net annual income — what lands in your bank account after all withholdings

Both numbers matter. They just matter for different things.

📌 Annual income can be measured by calendar year (Jan 1–Dec 31) or fiscal year, depending on your employer or tax situation. For most individuals in the U.S., the calendar year is standard.

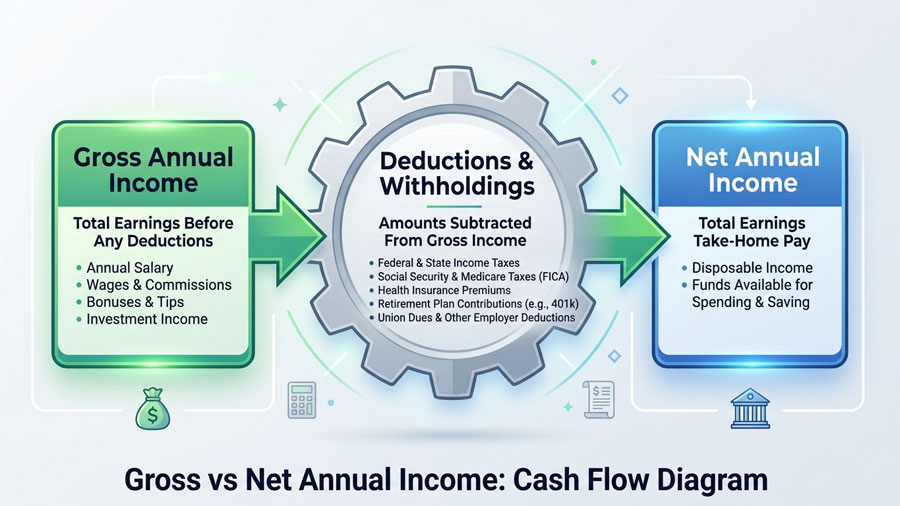

Gross vs. Net Annual Income: What’s the Real Difference?

Gross Annual Income

Gross annual income is your total earnings before a single dollar is withheld. This is the number on your offer letter, the figure banks ask for on loan applications, and the starting point for calculating your tax bracket.

It includes:

- Base salary or wages

- Overtime pay

- Bonuses and commissions

- Tips

- Self-employment revenue

- Investment income (dividends, capital gains)

- Rental income

Net Annual Income

Net annual income is what’s left after federal and state taxes, Social Security (6.2%), Medicare (1.45%), health insurance premiums, and retirement contributions are deducted. This is your actual take-home pay — the number that should drive every budgeting decision you make.

Why the Gap Is Bigger Than Most People Expect

Here’s what that $72,000 salary actually looks like in two different states:

| Texas (No State Income Tax) | California (Up to 9.3% State Tax) | |

|---|---|---|

| Gross Annual Income | $72,000 | $72,000 |

| Federal Income Tax (est.) | ~$10,300 | ~$10,300 |

| State Income Tax | $0 | ~$3,900 |

| FICA (SS + Medicare) | ~$5,508 | ~$5,508 |

| Estimated Net Income | ~$56,192 | ~$52,292 |

Estimates based on 2025 tax rates for a single filer with standard deduction. Actual amounts vary.

2025 federal tax brackets and standard deduction amounts

Same gross income. Nearly $4,000 difference in take-home pay — just from geography. This is why blanket budgeting advice (“spend 30% on housing”) often fails people: the math only works when you start from net, not gross.

⚠️ Common mistake: Building your monthly budget around your gross salary is one of the fastest ways to overspend. Always plan from net.

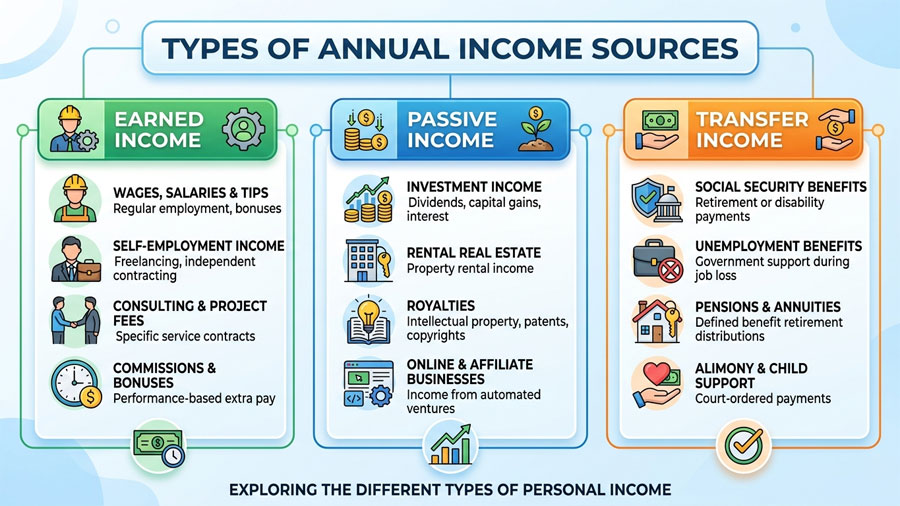

What Counts as Annual Income? (More Than Just Your Salary)

This is where many people leave money — or accuracy — on the table.

Earned Income

Your primary job: W-2 wages, hourly pay, salary, overtime, bonuses, commissions, and tips. If you work for it directly, it’s earned income.

Self-Employment and Freelance Income

Any 1099 income, consulting fees, gig economy earnings (Uber, Fiverr, Upwork), or side business revenue. Note: self-employed individuals also pay self-employment tax of 15.3% on net earnings — a detail that catches many first-time freelancers off guard.

Passive and Investment Income

Dividends, interest, rental income, capital gains, and royalties. These are taxed differently than earned income in many cases, which affects your effective rate.

Government and Benefit Income

Social Security benefits, disability payments, unemployment compensation, and pension distributions. These are often partially or fully taxable depending on your total income level.

Other Sources Lenders May Count

Alimony (for agreements finalized before 2019), child support, and trust distributions may count toward qualifying income for mortgage and loan applications.

qualifying income guidelines for conventional and FHA loans

How to Calculate Annual Income — By Employment Type

Salaried Employees

Formula: Gross Salary + Bonuses + Other Compensation = Gross Annual Income

Steps:

- Find your gross pay on your most recent pay stub (before deductions)

- Multiply by pay periods: ×52 (weekly), ×26 (biweekly), ×24 (semi-monthly), ×12 (monthly)

- Add expected annual bonuses or commissions

- Subtract annual deductions to get net annual income

Example: $5,500/month gross × 12 = $66,000 gross annual income. After ~$14,000 in taxes and deductions (varies by state and elections), net income lands around $52,000.

Hourly Workers

Formula: Hourly Rate × Avg. Weekly Hours × 52 = Gross Annual Income

Steps:

- Confirm your hourly rate from your pay stub or employment agreement

- Calculate your average weekly hours over the last 2–3 months

- Multiply: rate × hours × 52

- Adjust for unpaid weeks, seasonal changes, or known gaps

Example: $22/hour × 38 hours/week × 52 weeks = $43,472 gross annual income

Self-Employed and Freelance Workers

Formula: Total Revenue − Business Expenses = Net Business Income

Then subtract self-employment tax (15.3% on 92.35% of net earnings) and any estimated state taxes.

This calculation is more complex — income fluctuates, deductible expenses vary, and quarterly estimated tax payments are required. Track every income source and every legitimate business expense. [内链建議:self-employed tax deductions checklist → Tax Planning Guide page]

Example: $90,000 in freelance revenue − $18,000 in business expenses = $72,000 net business income. After SE tax (~$10,186) and federal income tax, actual take-home is closer to $52,000–$55,000.

Multiple Income Sources

This is where most calculators fall short. If you’re working a W-2 job and running a side business and collecting rental income, you need to combine all three streams carefully — each is taxed differently.

| Income Source | Amount | Tax Treatment |

|---|---|---|

| W-2 Salary | $58,000 | Ordinary income tax |

| Freelance Income | $18,000 | + SE tax (15.3%) |

| Rental Income | $9,600 | Ordinary income (after deductions) |

| Total Gross | $85,600 | Multiple rates apply |

Combining income sources without accounting for the different tax treatments leads to nasty surprises at filing time. A CPA or tax software that handles multi-source income is worth every dollar.

how debt-to-income ratio affects your mortgage approval

Annual Income and Taxes: What You Need to Know

Marginal vs. Effective Tax Rate

Your marginal rate is the rate on your last dollar of income — what most people mean when they say “I’m in the 22% bracket.” Your effective rate is your actual average rate across all income. For most middle-income earners, the effective federal rate runs between 12%–18%, well below the marginal rate.

This distinction matters because moving into a higher bracket doesn’t mean all your income is taxed at that rate. Only the dollars above the threshold are.

Key Deductions That Lower Taxable Income

- Standard deduction (2025): $15,000 (single) / $30,000 (married filing jointly)

- 401(k) contributions: Up to $23,500 pre-tax (2025 limit) — reduces taxable income dollar-for-dollar

- HSA contributions: $4,300 (self-only) / $8,550 (family) in 2025 — triple tax advantage

- IRA contributions: Up to $7,000 (or $8,000 if 50+)

Maximizing these accounts is one of the most direct ways to reduce your taxable annual income without earning less.

Frequently Asked Questions

Q: What is considered a good annual income in the U.S.?

The U.S. Census Bureau reported a median household income of approximately $80,610 in 2023. For individuals, the median was around $42,000. “Good” is relative to your cost of living, family size, and financial goals — but these figures give a useful benchmark.

Q: Is annual income the same as annual salary?

No. Annual salary is just one component of annual income. Annual income includes your salary plus any bonuses, freelance earnings, investment income, rental income, or other sources you receive in a year.

Q: Does annual income include bonuses?

Yes — gross annual income includes all bonuses, commissions, and supplemental pay. When reporting income for a loan application, lenders typically want to see a two-year history of bonus income before they’ll count it as reliable.

Q: What annual income do I need to qualify for a mortgage?

Lenders generally look for a debt-to-income (DTI) ratio below 43%. That means your total monthly debt payments — including your new mortgage — should not exceed 43% of your gross monthly income. For a $400,000 home with a 20% down payment, you’d typically need a gross annual income of at least $75,000–$90,000, depending on your other debts and current interest rates.

Q: How do I calculate annual income if I just started a new job?

Multiply your gross pay from one paycheck by the number of pay periods in a year. For a biweekly paycheck of $2,500: $2,500 × 26 = $65,000 gross annual income. If you started mid-year, note that this projects your full-year rate — your actual income earned this year will be lower.

Q: How is annual income verified for a loan application?

Lenders typically require W-2s from the past two years, recent pay stubs (last 30 days), and federal tax returns. Self-employed applicants usually need two years of tax returns, profit and loss statements, and sometimes bank statements.

The Bottom Line

Annual income isn’t just a number on a form. It’s the engine behind your budget, your borrowing power, your tax bill, and your retirement timeline. Understanding both your gross and net figures — and knowing exactly what flows into each — puts you in control of decisions that compound for decades.

Start with an honest calculation of every income source. Then work from your net number. Everything else follows from there.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax laws and income thresholds change annually. Consult a licensed CPA, financial advisor, or tax professional for guidance specific to your situation.