📋 Editorial Note: This article is for informational purposes only and does not constitute tax, legal, or financial advice. All figures reflect IRS guidance current as of 2026. Consult a licensed CPA or Enrolled Agent for advice specific to your situation.

Introduction

If your income crosses $200,000 this year, the additional Medicare tax is no longer something you can ignore. Most high earners know about it — few actually understand how it’s calculated, when their employer starts withholding it, or what happens when a spouse’s income pushes a couple over the threshold. This guide breaks down the 2026 rates, real calculation examples, Form 8959 basics, and legal strategies to manage your exposure. No fluff. Just what you need.

What Is the Additional Medicare Tax?

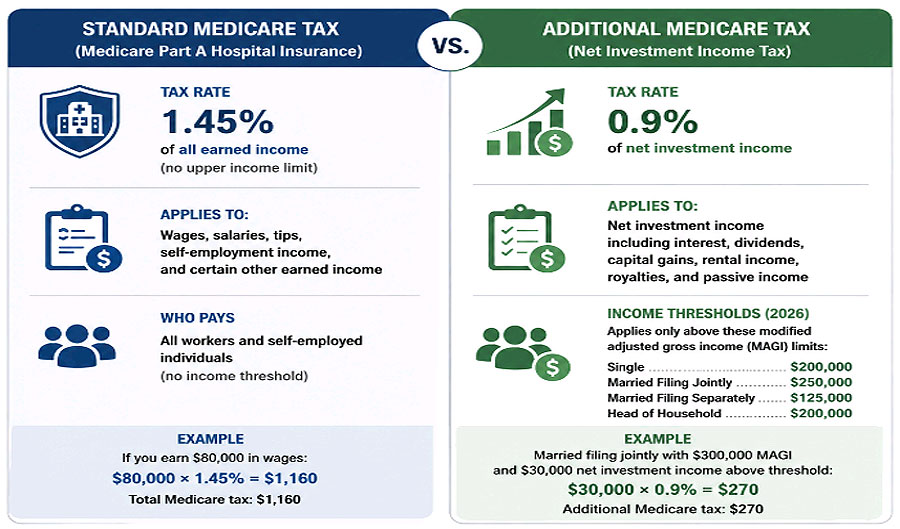

The Additional Medicare Tax is a 0.9% surtax on earned income above IRS-set thresholds. Congress created it under the Affordable Care Act (ACA), effective January 1, 2013.

Two things most people get wrong immediately:

- It does not fund Medicare Part A. The revenue goes toward ACA premium tax credits — the subsidies that help lower-income Americans buy health coverage on the federal marketplace.

- Your employer does not match it. The standard Medicare tax splits 1.45%/1.45% between employee and employer. This extra 0.9%? It’s yours alone.

2026 Income Thresholds: The Numbers That Matter

The thresholds have not changed since 2013. They are not indexed to inflation — a deliberate policy choice that quietly pulls more middle-to-high earners into the tax each year.

| Filing Status | 2026 Income Threshold | Additional Tax Rate |

|---|---|---|

| Single / Head of Household | $200,000 | 0.9% |

| Married Filing Jointly (MFJ) | $250,000 | 0.9% |

| Married Filing Separately (MFS) | $125,000 | 0.9% |

| Qualifying Widow(er) | $250,000 | 0.9% |

💡 Worth noting: The Tax Policy Center estimates that the number of households affected by this tax has grown steadily since 2013 — not because of rate changes, but because wages have risen while thresholds stayed flat.

IRS official guidance on Additional Medicare Tax thresholds

Who Actually Owes This Tax?

W-2 Employees

Your employer is required to start withholding the extra 0.9% once your wages from that employer exceed $200,000 in a calendar year. This applies regardless of your filing status or your spouse’s income.

That creates a gap. If you earn $180,000 and your spouse earns $120,000, neither employer withholds a dime — but your combined $300,000 exceeds the $250,000 MFJ threshold. You still owe the tax. You just have to calculate and pay it yourself at filing.

Self-Employed Individuals

Self-employed filers pay the full 2.9% standard Medicare tax (no employer to split it with), plus the additional 0.9% on income above $200,000. That’s 3.8% on the excess — and no one is withholding it for you.

One rule that trips people up: a self-employment loss cannot reduce your Additional Medicare Tax base. If your day job pays $190,000 and your side business clears $20,000 after expenses, you owe the tax on $10,000 — even if another venture had a loss.

how self-employed individuals calculate and pay quarterly estimated taxes

Married Couples: The Scenarios That Cause the Most Confusion

| Scenario | Spouse A | Spouse B | Combined | Filing | Owe Tax? | Withheld? |

|---|---|---|---|---|---|---|

| High/low earner | $225,000 | $10,000 | $235,000 | MFJ | ❌ No | ✅ On $25K |

| Dual income | $150,000 | $150,000 | $300,000 | MFJ | ✅ Yes ($50K) | ❌ Neither |

| MFS filer | $130,000 | N/A | $130,000 | MFS | ✅ Yes ($5K) | ❌ No |

The Married Filing Separately trap deserves special attention. The $125,000 threshold exists specifically to prevent couples from using separate returns to dodge this tax. If you’re considering MFS for any reason, run the numbers carefully — the lower threshold often makes it worse, not better.

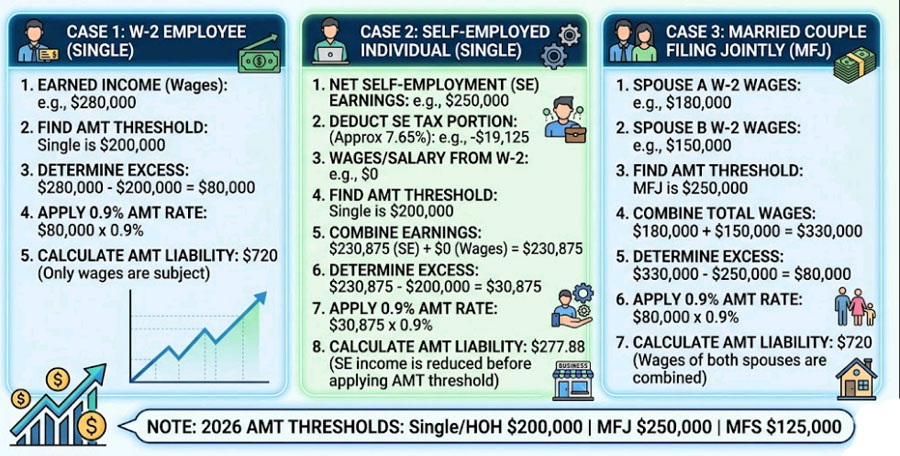

How to Calculate Your Additional Medicare Tax (Step-by-Step)

Example A: Single W-2 Employee

- Annual wages: $230,000

- Threshold: $200,000

- Taxable excess: $30,000

- Tax owed: $30,000 × 0.9% = $270

Your employer already withheld this on the $30,000 above $200,000. No additional action needed if your total income matches.

Example B: W-2 + Freelance Income

- W-2 wages: $180,000

- Net self-employment income: $60,000

- Combined total: $240,000

- Threshold: $200,000

- Taxable excess: $40,000

- Tax owed: $40,000 × 0.9% = $360

Your employer withheld nothing (wages stayed under $200,000). You must calculate this on Form 8959 and pay at filing — or make quarterly estimated payments to avoid a penalty.

Example C: Married Couple, Dual Income

- Spouse A wages: $150,000 | Spouse B wages: $150,000

- Combined: $300,000 | MFJ threshold: $250,000

- Taxable excess: $50,000

- Tax owed: $50,000 × 0.9% = $450

Neither employer withheld anything. This $450 shows up as a balance due on the joint return — and if you didn’t make estimated payments, you may also owe a small underpayment penalty.

Form 8959: How to Report It

Form 8959 is the one-page IRS form you attach to your Form 1040 to calculate and report your Additional Medicare Tax. You file it when your combined wages, self-employment income, or RRTA compensation exceeds the threshold for your filing status.

Key lines to know:

| Line | What You Enter |

|---|---|

| Lines 1–3 | Wages, unreported tips, RRTA compensation |

| Line 4 | Total earned income |

| Line 5 | Your applicable threshold |

| Line 6 | Excess income (Line 4 minus Line 5) |

| Lines 7–10 | Self-employment income adjustments |

| Line 18 | Total Additional Medicare Tax — transfers to Form 1040 |

Three common mistakes on Form 8959:

- Forgetting to include self-employment income in the combined total

- Using a self-employment loss to reduce the tax base (not allowed)

- Confusing this form with Form 8960 — that’s for the Net Investment Income Tax (NIIT), which is a separate 3.8% tax on passive investment income

official Form 8959 and line-by-line instructions

Legal Ways to Reduce Your Exposure

You cannot avoid this tax if you earn above the threshold. But you can manage your taxable income with legitimate planning:

Max out tax-deferred retirement accounts. Contributions to a 401(k), SEP-IRA, or Solo 401(k) reduce your adjusted gross income. A single filer contributing $23,000 to a 401(k) shifts their effective threshold exposure down by exactly that amount.

If you own a business, time your income. Ask clients to pay Q4 invoices in January if your income is running high. Accelerate deductible equipment purchases under Section 179 in the current tax year.

Fix your W-4 if you’re in a dual-income household. If neither spouse earns over $200,000 but your combined income exceeds $250,000, no withholding happens automatically. Use Line 4(c) on Form W-4 to request additional withholding — or make quarterly estimated payments using Form 1040-ES.

⚠️ Important: These are standard tax planning strategies. Before implementing any of them, review with a licensed CPA or Enrolled Agent who knows your full financial picture.

Frequently Asked Questions

Is the Additional Medicare Tax the same as the Medicare surtax?

Yes. “Medicare surtax,” “Additional Medicare Tax,” and “0.9% Medicare tax” all refer to the same levy. The terms are used interchangeably.

Does the Additional Medicare Tax apply to Social Security or investment income?

No. It applies only to earned income — wages, tips, and self-employment income. Investment income (dividends, capital gains, rental income) falls under the separate 3.8% Net Investment Income Tax if you exceed the same thresholds.

What if my employer withholds too much?

If your employer withholds the 0.9% but your actual liability (based on filing status and total household income) is lower, the excess is credited against your total tax bill when you file. You won’t lose it.

Will the $200,000 threshold ever be adjusted for inflation?

As of 2026, no. The ACA did not include an inflation adjustment for these thresholds. Any change would require an act of Congress.

Bottom Line

The Additional Medicare Tax is straightforward once you understand the rules. The 0.9% rate applies to earned income above $200,000 (single) or $250,000 (married filing jointly). Employers withhold based on individual wages only — which means millions of dual-income couples owe tax their employers never touched. Self-employed filers carry the full calculation burden themselves.

If your income is near or above these thresholds, check your withholding now — not in April.

📋 Disclaimer: This content is provided for general informational purposes only and does not constitute tax, legal, or financial advice. Tax laws are subject to change. Individual circumstances vary. Always consult a licensed CPA, tax attorney, or IRS Enrolled Agent before making tax-related decisions.