Your landlord won’t accept a personal check. The car seller wants guaranteed funds. Suddenly, you’re choosing between a money order vs cashier’s check — and the wrong pick could cost you time, money, or the deal itself.

Both instruments guarantee payment. But they work differently, cost differently, and suit very different situations. This guide breaks down the real fees, legal limits, fraud risks, and a decision tool so you can choose in under 30 seconds.

Key Takeaways

- Money orders: max $1,000, no bank account needed, fees start at $1

- Cashier’s checks: no dollar limit, bank account usually required, fees run $8–$15

- For any transaction over $1,000 → cashier’s check is almost always the right call

- Both can be counterfeited — here’s exactly how to verify each one

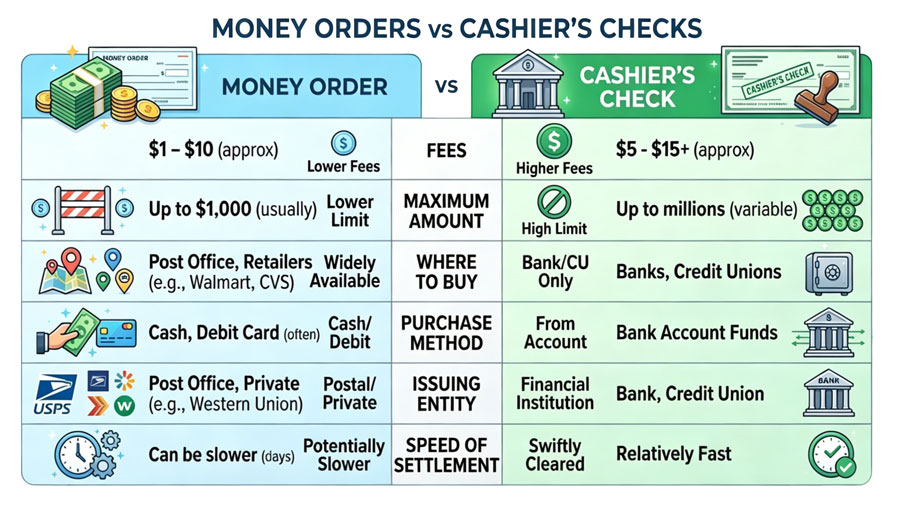

Money Order vs Cashier’s Check: Side-by-Side

| Feature | Money Order | Cashier’s Check |

|---|---|---|

| Max Amount | $1,000 | No limit |

| Bank Account Required | No | Usually yes |

| Where to Buy | USPS, Walmart, CVS, banks | Banks & credit unions only |

| Average Fee | $1–$5 | $8–$15 |

| Funds Available (Next Day) | First $200 | First $5,525 |

| Privacy | High | High |

| Best For | Rent, small purchases | Real estate, vehicles, large deposits |

Source: Federal Reserve Regulation CC; USPS official fee schedule (verified June 2026)

What Is a Money Order?

A money order is a prepaid paper payment — you hand over cash, get a slip worth exactly that amount, and the issuer guarantees it. No personal bank account. No routing numbers exposed.

That’s why roughly 4.5% of U.S. households — those without a traditional bank account — rely on money orders for everyday payments.

Where to Buy One (And What You’ll Actually Pay)

| Issuer | Max Per Order | Fee |

|---|---|---|

| USPS | $1,000 | $2.35 (≤$500) / $3.40 (≤$1,000) |

| Walmart / MoneyGram | $1,000 | $1.00 |

| Western Union | $1,000 | $1.50–$2.00 |

| CVS / Rite Aid | $500 | ~$1.25 |

| Chase / Bank of America | $1,000 | $5.00 |

USPS is the gold standard for a reason: postal money orders get the same next-day funds availability as cashier’s checks. Other issuers don’t get that treatment.

The $1,000 Ceiling — And the $3,000 Rule You Need to Know

Money orders cap at $1,000 per slip. Need $4,000? That’s four separate money orders — plus four separate fees.

Here’s what most guides skip: Under the Bank Secrecy Act, if you purchase more than $3,000 in money orders in a single day, the issuer is legally required to collect your government-issued ID and file a report. Bank Secrecy Act reporting requirements

Trying to split purchases across multiple locations to avoid this threshold? That’s called structuring — a federal offense under 31 U.S.C. § 5313, regardless of whether the underlying money is legitimate.

When a Money Order Makes Sense

- Monthly rent or security deposit under $1,000

- Paying someone who doesn’t have a bank account

- Government fees (court costs, permit applications)

- Private-party purchases where you don’t want to share banking details

What Is a Cashier’s Check?

A cashier’s check is issued and guaranteed by the bank itself — not by you personally. When you buy one, funds are pulled from your account immediately and held by the bank. The recipient gets the bank’s word (and the bank’s money) backing the payment.

That’s why real estate closings, car dealerships, and large landlords prefer them. A personal check can bounce. A legitimate cashier’s check essentially cannot.

how wire transfers compare to cashier’s checks for real estate closings

Cashier’s Check Fees by Bank — Real Numbers

This is where most comparison articles fall short. Here’s what major U.S. banks actually charge:

| Bank | Fee (Customer) | Fee (Non-Customer) | Available via App? |

|---|---|---|---|

| Chase | $8 | $10 | Yes |

| Bank of America | $15 | $20 | Branch only |

| Wells Fargo | $10 | Not offered | Branch only |

| U.S. Bank | $7 | $15 | Yes |

| Citibank | $10 | $20 | Branch only |

| Federal Credit Unions | Free–$5 | Varies | Varies |

Data sourced from bank official websites, June 2026. Fees subject to change — verify directly before visiting.

Can You Get a Cashier’s Check Without a Bank Account?

Yes, but it’s harder. Three options:

- Walk into a bank as a non-customer. Some branches (not all) will issue one for cash, usually at a higher fee. Call ahead.

- Use an online bank. Several will mail you a cashier’s check — useful if your bank has no local branch.

- Try a federal credit union. Many serve walk-in members of the public and charge lower fees.

When a Cashier’s Check Is the Right Call

- Home down payments and real estate closings

- Purchasing a vehicle over $5,000

- Court-ordered payments or bail bonds

- Any transaction where the payee explicitly requires guaranteed bank funds

Real Cost Comparison: The Math Most People Don’t Do

Say you need to pay $9,000 for a used car.

Money order route: 9 separate money orders at $3.40 each (USPS) = $30.60 Cashier’s check route: 1 check at $8–$10 (Chase customer) = $8–$10

For large amounts, cashier’s checks are often cheaper — not just more convenient. The “money orders are affordable” argument breaks down fast above $1,000.

Fraud and Scams: What You Actually Need to Check

Both instruments are common targets for fraud. The FTC received over 330,000 reports of check fraud in 2023, with fake cashier’s checks heavily represented.

The standard scam: someone sends you a cashier’s check (or money order) for more than you’re owed, asks you to deposit it and wire back the difference. The check fails — sometimes days later — and you’re liable for the full amount you wired out.

How to Verify a Cashier’s Check — Step by Step

- Call the issuing bank directly — use the number on the bank’s official website, not the one printed on the check

- Inspect physical features: legitimate checks include watermarks, color-shifting ink, and microprinting along borders

- Refuse any “deposit and return” request — no legitimate buyer or employer does this

- For USPS money orders, call the Money Order Verification System: 1-877-876-2455

If Your Payment Goes Missing

- Money order lost: Keep your receipt → file USPS Form 6401 → expect 30–60 days for resolution

- Cashier’s check lost: Submit an indemnity bond to your bank → mandatory 90-day waiting period before reissuance (per UCC § 3-312)

The cashier’s check process is more expensive and slower. Keep copies of everything.

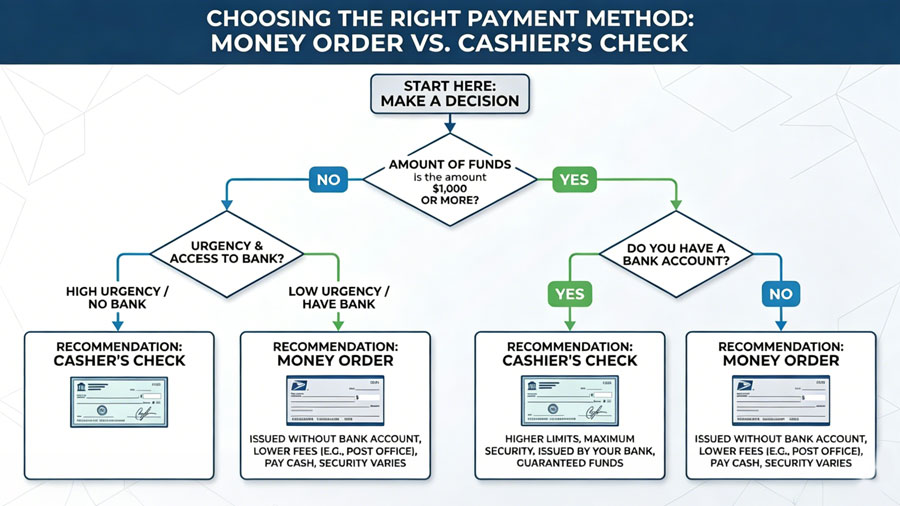

30-Second Decision Guide: Which One Do You Need?

Answer two questions:

1. Is the amount over $1,000?

- No → Money order works. If you have no bank account, it’s your only real option.

- Yes → Go with a cashier’s check.

2. Does the payee specify which one they want?

- Always follow their requirement. A landlord who requires a money order won’t accept a cashier’s check as a substitute.

| Situation | Best Choice |

|---|---|

| Rent or deposit under $1,000 | Money order |

| Buying a car or property | Cashier’s check |

| No bank account | Money order |

| Payee requires bank guarantee | Cashier’s check |

| Craigslist or private sale | Either — verify first |

FAQ: Money Order vs Cashier’s Check

Q1: Is a money order as good as a cashier’s check?

For amounts under $1,000 and everyday transactions, yes. For high-value purchases or when a seller specifically requires a bank guarantee, no — a cashier’s check carries more weight.

Q2: What happens if a cashier’s check bounces?

A legitimate cashier’s check from a real bank won’t bounce. If one does, it’s almost certainly counterfeit. Contact your bank and local law enforcement immediately — don’t send any funds.

Q3: Do money orders expire?

USPS money orders don’t technically expire, but non-USPS issuers (Western Union, MoneyGram) may charge dormancy fees after 1–3 years. Check the issuer’s terms when you buy.

Q4: Can I cancel a money order or cashier’s check?

Yes, but neither is quick. Money orders require a waiting period and a fee. Cashier’s checks involve a 90-day indemnity process. If the recipient has already cashed it, cancellation isn’t possible.

Q5: What’s the safest way to send money for a large purchase?

For amounts over $10,000, a wire transfer or cashier’s check from a major bank offers the strongest protections. Wire transfers are faster but non-reversible. Cashier’s checks give both parties a paper trail.

The Bottom Line

The money order vs cashier’s check decision comes down to three factors: how much you’re paying, whether you have a bank account, and what the recipient will accept. For small payments and everyday transactions, money orders are fast, cheap, and accessible. For anything large, a cashier’s check is the cleaner, often cheaper, and universally accepted option.

Whichever you choose — verify before you trust it.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or professional advice. Fee information reflects publicly available data as of June 2026 and is subject to change. For guidance specific to your situation, consult a licensed financial advisor or legal professional.